#MonetaryPolicy101 is a weekly series about the basics of monetary policy. This is the seventh post. See Post 1 here, Post 2 here, Post 3 here, Post 4 here, Post 5 here and Post 6 Here. If you like this series please consider taking out a paid subscription here.

Last week, I wrote about the plumbing of payments and how its the payment system itself that makes money socially valuable- in fact its the payment system itself that is money. The week before that I wrote about how banks have a payment processing role and this gives them leverage over their customers that they wouldn’t otherwise have. The open question remains- how do banks get this privileged place in the payments system which allows them to emit money? The answer is in some ways simple and in some ways quite complex: they get a license to issue money.

This should seem simple. Isn’t it obvious that you would need a license to become a bank? Yet, its unsettling to our shared conventional approach to banks to think about this because it disrupts our ability to view banks as purely private entities. When I say “bank” your immediate thought is not “entity with obligation to the general public”. Its usually some capricious activity that they’ve engaged in (especially over the last decade) or their staggering profitability and size. If their power is a privilege granted by our legal system, surely we can change how they behave? The answer to that question is yes. To get more of a handle on this point, lets go through a helpful page on the Federal Reserve’s website which answers the simple question “How Can I Start a Bank”?

Starting a bank involves a long organization process that could take a year or more, and permission from at least two regulatory authorities. Extensive information about the organizer(s), the business plan, senior management team, finances, capital adequacy, risk management infrastructure, and other relevant factors must be provided to the appropriate authorities.

The proposed bank must first receive approval for a federal or state charter. The Office of the Comptroller of the Currency (OCC) has exclusive authority to issue a federal or "national bank" charter, while any state (and the District of Columbia, Guam, Puerto Rico, and the Virgin Islands) may issue a state charter. Before granting a charter, the OCC or state must be able to determine that the applicant bank has a reasonable chance for success and will operate in a safe and sound manner. Next, the proposed bank must obtain approval for deposit insurance from the Federal Deposit Insurance Corporation (FDIC). Additional approvals are required from the Federal Reserve if, at formation, a company would control the new bank and/or a state-chartered bank would become a member of the Federal Reserve.

All insured banks must comply with the capital adequacy guidelines of their primary federal regulator (Federal Reserve, FDIC, or OCC). The guidelines require a bank to demonstrate that it will have enough capital to support its risk profile, operations, and future growth even in the event of unexpected losses. Newly established banks are generally subject to additional criteria that remain in place until the bank's operations become well-established and profitable.

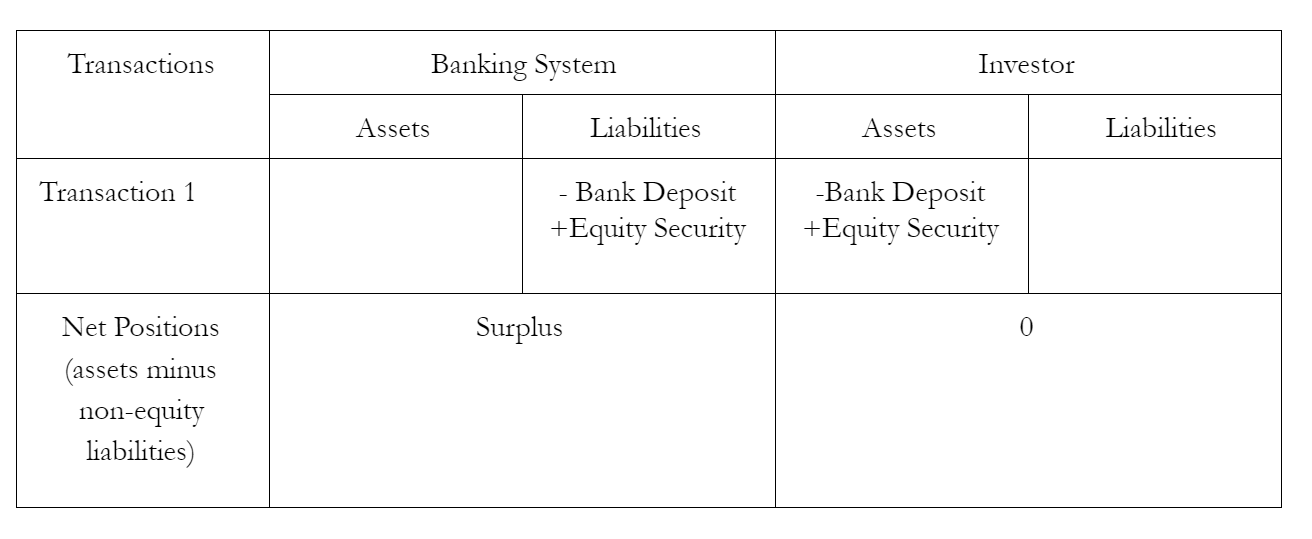

Let’s break that down step by step. To get a bank license you can’t just say “I want a bank!”. You have to have a specific business plan, meaning written strategy documents detailing specific areas of the banking business you would enter, who you would hire to run the bank, how you would manage risks and other operational questions and so on. Most importantly though, you need to line up investors. That’s what “capital adequacy” means. It means you have people or entities willing to buy equity securities in your potential bank who will receive dividends (and potentially capital gains) to compensate them for the possibility that they will take capital losses. This is a very important point, so let’s dig deeper into it.

Equity securities are a special type of liability because the obligation it creates towards one’s creditors is unique. A company has an “obligation” to pay an equity holder dividends if it pays dividends, but the company doesn’t have an actual obligation to pay dividends to shareholders in general. Instead, companies have an obligation to give shareholders a vote in specific important company decisions and for members of the board of directors of the company. Because this is a different type of liability, its treated differently in accounting. In this series I’ve been drawing T accounts which say “assets” on one side and “liabilities” on the other. I will keep on doing that, but keep in mind that these are unique types of liabilities. Because these types of liabilities are not debt liabilities, their sale to investors increases the net worth of a bank for the purposes of bank regulation without decreasing the net worth of the investors.

Notice that the financial assets and financial liabilities here don’t sum to zero. How can this be the case when every financial asset must be matched by a financial liability? This principle is also true here. What’s different in this circumstance is that “net positions” are excluding equity liabilities, but including equity assets since stocks are generally treated as a type of financial asset. This uneven treatment leads to surpluses and deficits depending on whether equity liabilities are being net issued or net retired. Nonetheless, this uneven treatment is an important feature of legal and financial reality. Its also important to remember that the payment the investor is most likely making does not involve some kind of “outside” money such as central bank settlement balances or gold. Today, the “money” they are paying with is most likely a bank deposit balance held with another bank. This is where the “equity” of a bank comes from. For the banking system as a whole, one type of liability is simply being swapped for another. Consolidating the banking system together will make this point clearer.

Let’s return to the Federal Reserve’s handy description of how to form a bank. So you’ve lined up the investors who are going to help you conjur up some financial net worth to meet capital requirements. You have a business plan and prospective staff. Now its time to obtain a charter itself. In our federalist system, prospective bankers have a choice of obtaining a bank charter from the Office of the Comptroller of the Currency, a bureau of the United States Treasury, or a state regulator. If all they want is a state charter, things end there. However, a major modern legal privilege banks obtain is deposit insurance. This is a federal government guarantee that checking and saving account liabilities will retain 100% of their value, even if the bank take large losses and end up having a negative net worth. In times without deposit insurance there was not a superior form of retail money that prospective bank customers would have access to. This made the lack of deposit insurance less of a problem for banks, though it was still a problem. I will return to this topic next week. However, today it is a major problem for a state chartered bank to not have federal deposit insurance as it makes their liabilities inferior to the more common form of retail money. Thus, banks are most likely going to seek Federal Deposit Insurance Corporation insurance.

Finally, banks also have the choice of being a Federal Reserve member bank. This gives them direct access to the Federal Reserve’s payment system and direct access to the discount window i.e. direct borrowing from the Federal Reserve. When times are bad, banks greatly value direct access to the Federal Reserve’s lending facilities. When times are good, banks get increasingly comfortable with indirect access and will forgoe Federal Reserve membership to avoid liquidity requirements. This became a significant problem by the 1970s and led to congress changing the law in the “Monetary Control Act of 1980” to impose liquidity requirements on all banks, whether or not they are Federal Reserve member banks. Later in the series I will discuss liquidity requirements in more detail. To sum up, people and companies looking to set up a bank have a series of choices in front of them that impact what legal privileges and obligations they will incur. If you choose to obtain a Federal licesnse, you are subject to the Office of the Comptroller of the Currency’s regulation. If you seek deposit insurance, you’re subject to the Federal Deposit Insurance Corporation’s regulations, but also have access to deposit insurance. If you seek to become a Federal Reserve member bank, you incur the obligations but also gain the rights that that involves. The paridgmatic modern U.S. bank is both a Federal Reserve member bank and has access to federal deposit insurance.

What’s confusing about this process is that no federal or state regulator will straightforwardly tell a bank that they are obtaining a license to create money. Instead, they are gaining a set of legal privileges that amount to the ability to create money because of their unique access to the payments system and the privileged sources of short-term credit that licensed banks have. It wasn’t always so complicated. In the era between the signing of the U.S. constitution and the civil war, known as the Antebellum period, bank charters would simply straightforwardly say that the bank notes that state chartered banks issued would be acceptable in payment for taxes and other “public dues”. Take, for example this 1835 South Carolina Bank Charter to incorporate "The Bank of Camden, South Carolina":

That the bills or notes of the said corporation originally made payable on demand, or which shall become payable in gold or silver current coin, shall be receivable by the treasurers, tax collectors, and solicitors, and other public officers, in all payments for taxes, or other monies, due to the State, so long as said Bank shall pay gold and silver current coin for their notes; but whenever there shall be a protest on any of the bills or notes of said Bank for non-payment in specie, the Comptroller General shall be authorized, and he is hereby required, to countermand the receipt of the bills or notes of the Bank in payment of taxes, or debts due to the State, unless good and satisfactory cause shall be shown him, by the said corporation, for contesting in a court of justice the payment thereof

This is a much more straightforward way of understanding the rights and privileges of banks. The public is granting a bank’s liabilities general acceptability, and in return they should serve some useful public purpose. This reframing also challenges a lot of our conventional understanding of banks. Repealing their social obligations does not reduce government intervention. It expands what putatively private actors can do using the powers granted to them by public law. For example, if capital requirements were repealed and banks were allowed to spend and grant far more than their income, we’d essentially be licensing out to them the fiscal power to deficit spend. Its obvious that their gobbling up of society’s resources using this new found power is not some “free market” being put into operation. We, in fact, would experience it as an extraordinary intervention into the functioning of the economy. While this is an extreme case, this is true about any loosening of regulations on licensed banks. Just like McDonalds franchises, banks are the government’s franchise. If McDonald’s loosened quality standards on its franchisees, we’d rightly see their subsequent actions as Mcdonalds’ responsibility. The same goes for alleged “deregulation” of banks.

That’s all for today! See you next week where we will explore “liquidity crises”.